<< NOTE: The link to download the complete "Operator Advantage in Venture Capital" white paper appears at the end of this blog post.

The venture industry has spent years debating whether operator-led funds actually outperform — or whether it's just a good story. Sheila Trucco of Scientifica.ai decided to find out.

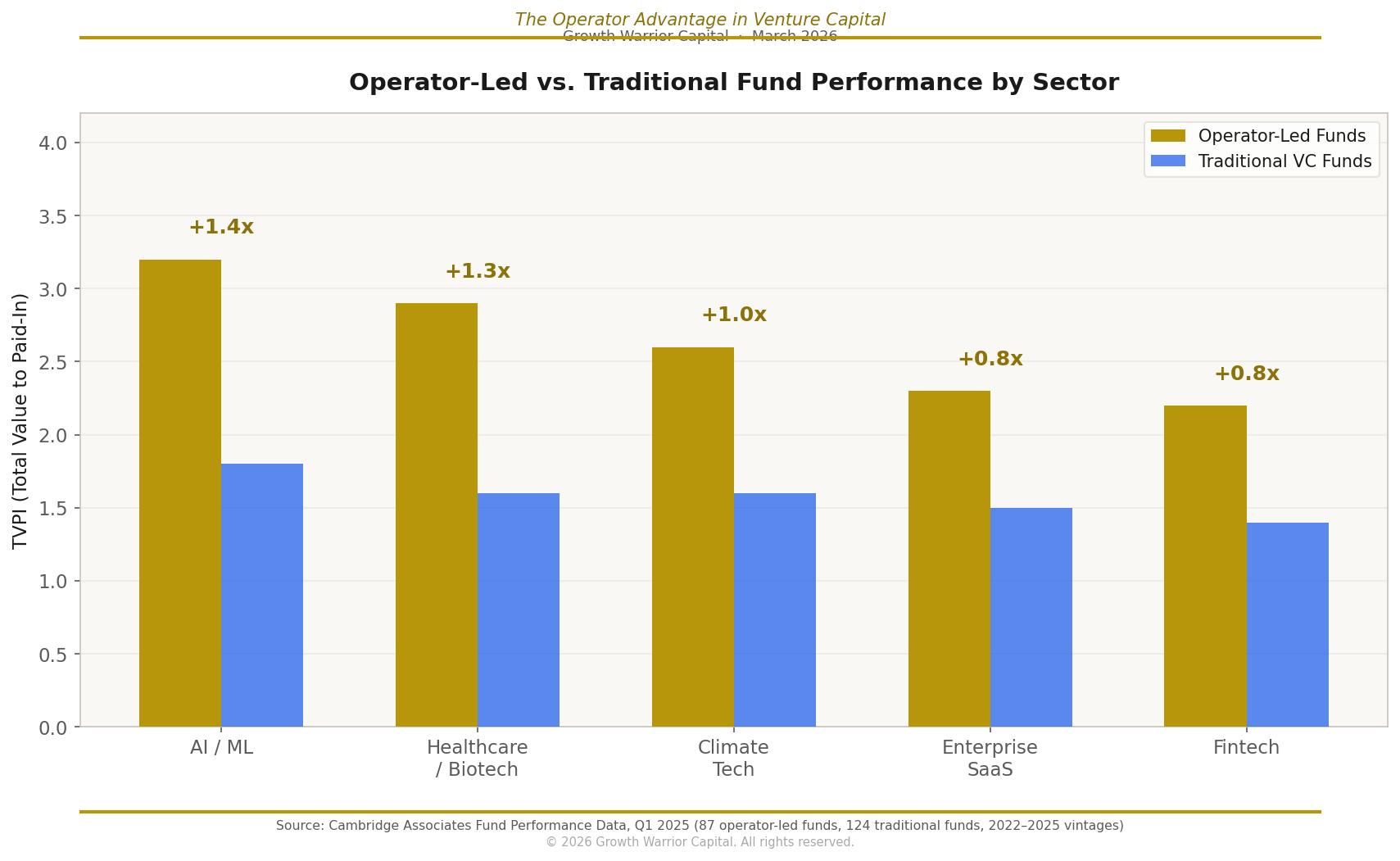

Her research drew from 87 operator-led funds and 124 traditional funds across 2022–2025 vintages, sourced from Cambridge Associates. The findings are unambiguous: Operator-led funds outperform traditional venture capital by 1.7x in early-stage returns.

We commissioned this research because we wanted the truth, not confirmation of a narrative we already believed. What Sheila found exceeded what we expected — not just in the headline number but in the precision of where and why the advantage exists.

This post walks through the full findings. If you want to go deeper, Sheila and GWC founder and managing director Promise Phelon sat down to discuss the research in full — watch the conversation here:

And if you want the complete white paper, you can download it directly at the bottom of this post.

The headline: 1.7x outperformance across the board

The 1.7x figure is the average across all sectors. But the data gets more interesting when you break it down by where the money is actually being deployed.

Operator-led funds investing in AI/ML generate a 3.2x TVPI versus 1.8x for traditional VCs. In healthcare and biotech, 2.9x versus 1.6x. Climate tech, 2.6x versus 1.6x. Enterprise SaaS, 2.3x versus 1.5x. Fintech, 2.2x versus 1.4x.

The pattern holds across every sector. But the outperformance is widest precisely where domain complexity is highest — where an investor who has never actually operated in the industry is working with a fundamental information disadvantage. The founders in these sectors know who's been in the room and who hasn't. The deals reflect it.

Scale kills returns every time

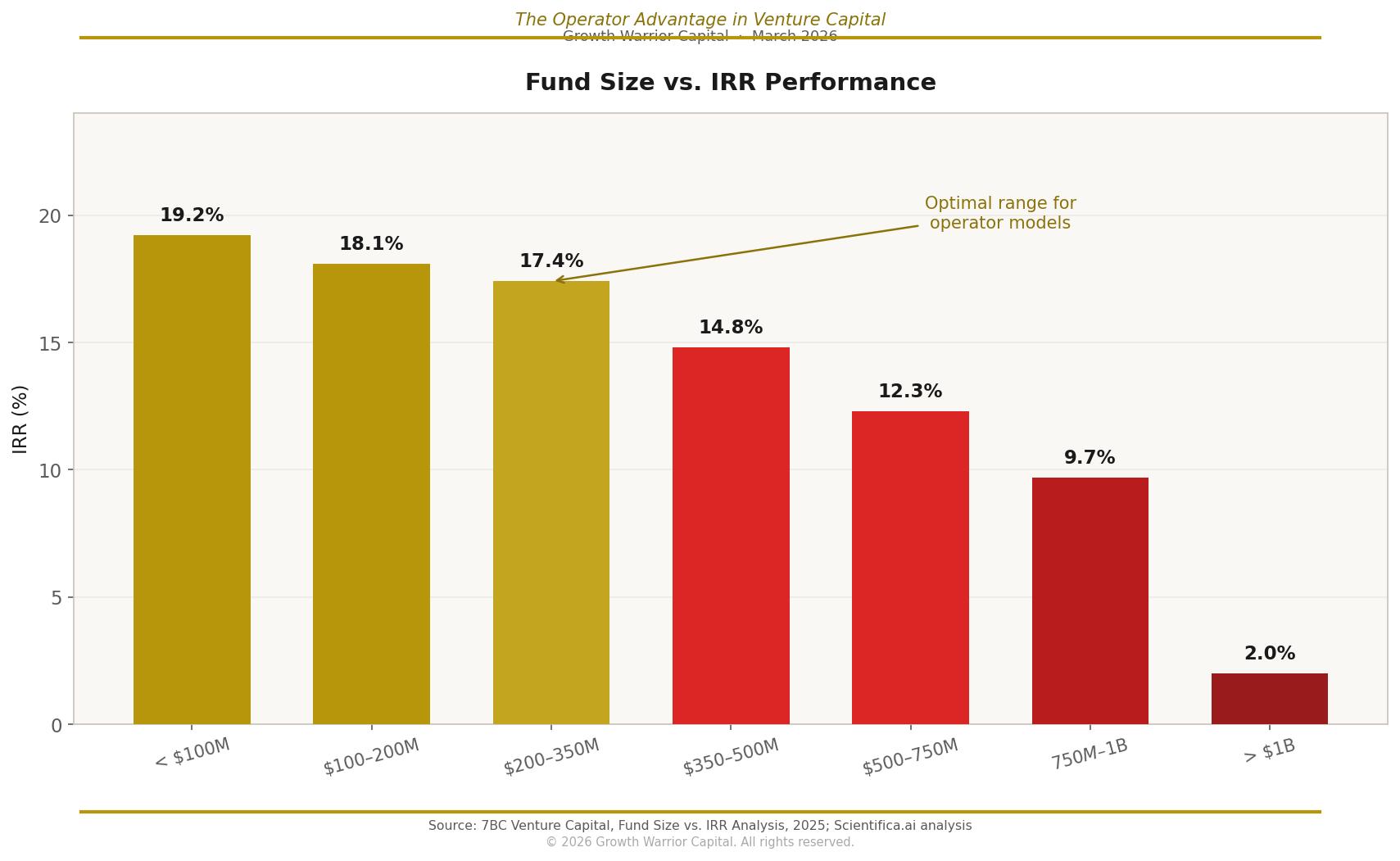

The second finding is one the industry doesn't talk about enough. Fund size is inversely correlated with IRR — and the relationship is steep.

Operator-led funds in the $50M–$350M range consistently generate the strongest IRR. Above $500M, returns erode sharply. Above $1B, the advantage nearly disappears. The math is straightforward: Smaller, focused funds move faster, price more precisely and stay operationally close to their companies. Larger funds optimize for capital deployment. Those are different objectives — and they produce different outcomes.

This is one of the most important and least discussed dynamics in venture. Institutional allocators chasing AUM concentration at the top of the market may be systematically trading return potential for the comfort of familiar brand names.

Five structural drivers — not luck, not timing

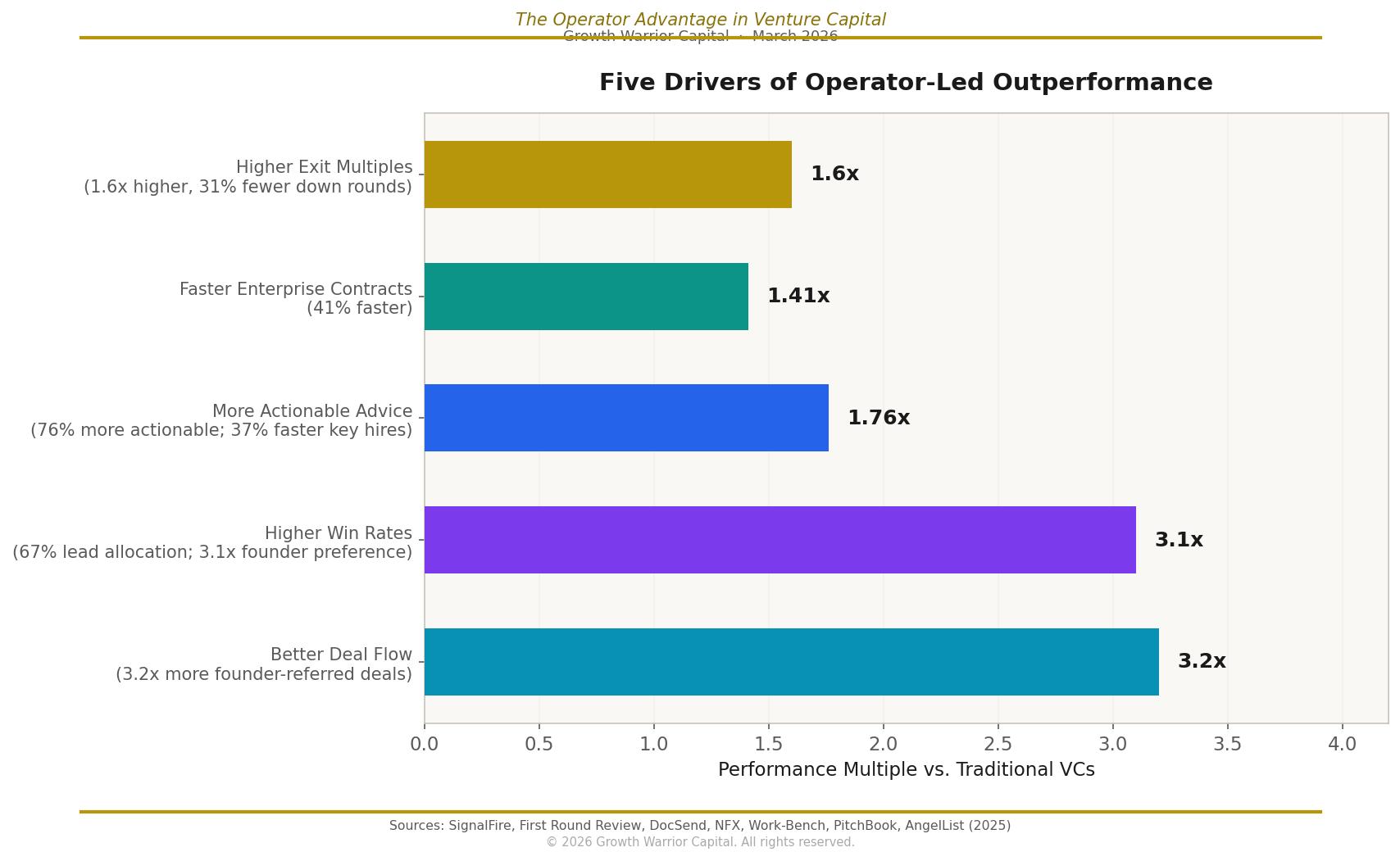

The 1.7x outperformance isn't a vintage anomaly. Sheila's research identifies five distinct structural drivers that explain why the gap exists and why it persists.

- Better deal flow. Operator-led funds source 3.2x more founder-referred deals. Founders talk to other founders. Proprietary deal flow is a byproduct of credibility.

- Higher win rates. When operators compete for a deal, founders choose them as lead 67% of the time. Experience is a more powerful signal than brand recognition when a founder is deciding who they want in their corner.

- More actionable advice. Portfolio companies report 76% more actionable guidance and hire key executives 37% faster. The difference between "I know someone" and "here's exactly how I solved this and here's who you need to call" compounds over time.

- Higher exit multiples. Operator-led funds achieve 1.6x higher exit multiples and see 31% fewer down rounds. Companies that get the right operational support at the right moment compound.

- Faster enterprise contracts. Portfolio companies close enterprise contracts 41% faster when backed by operators with relevant industry relationships. In sectors where sales cycles are long and trust is everything, this is a major advantage.

Each driver reinforces the others. The flywheel is real.

Founders already know about the operator advantage

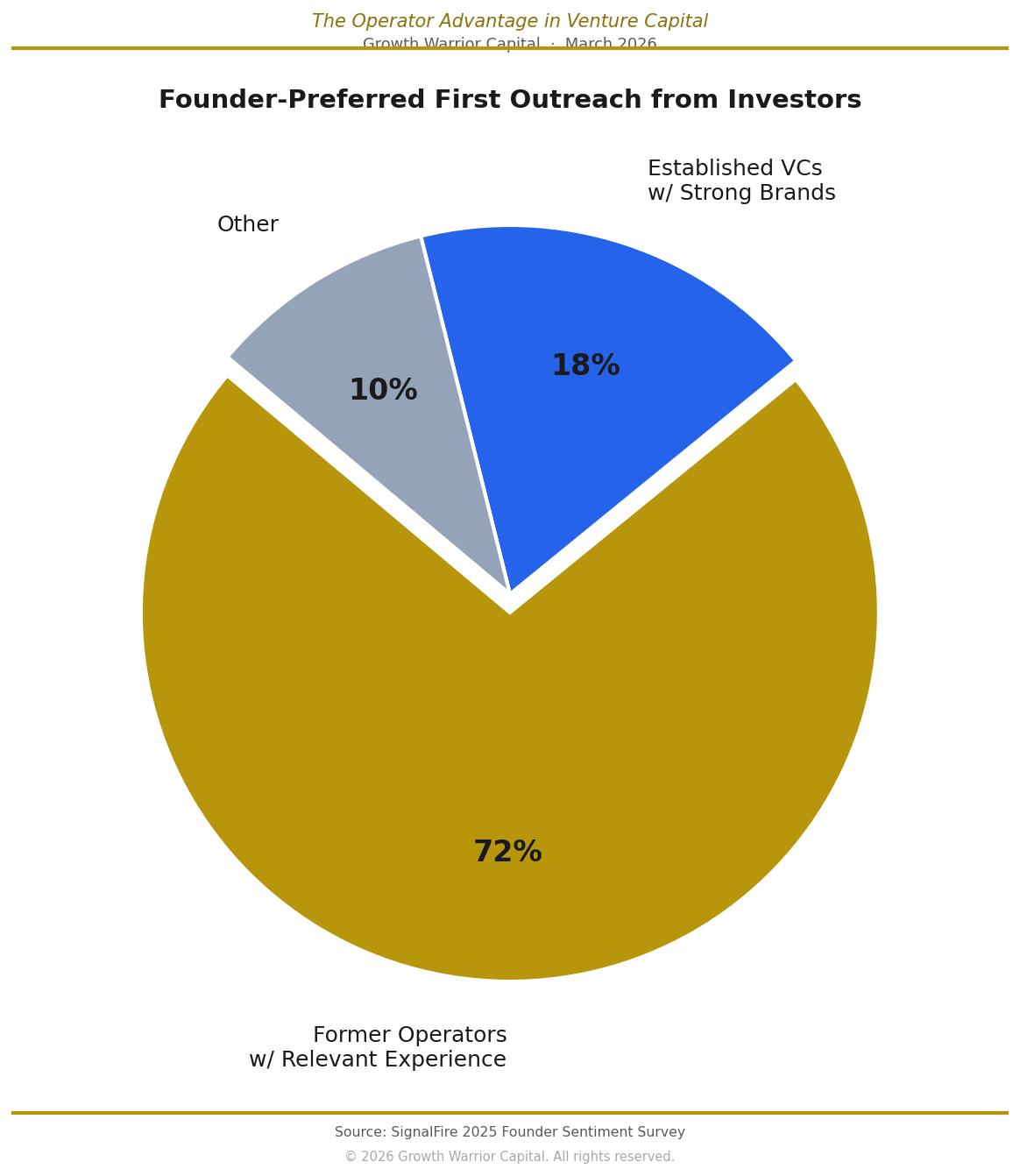

The research doesn't just validate the operator advantage from a returns perspective. It validates it from the founder's perspective, too.

Seventy-two percent of founders in operator-intensive sectors say their first choice for investor outreach is a former operator with relevant experience. Established VCs with strong brand names? Eighteen percent. The founders building the hardest companies in the hardest industries have already made their judgment. They want someone who's been where they're trying to go.

Proof over proximity. Every time.

The 4D Economy: Where the advantage is greatest

GWC's thesis has always been that the operator advantage is most pronounced in what we call the 4D Economy — sectors with Dirty, Dull, Dangerous and Dated jobs. Manufacturing, logistics, agriculture, supply chain. In these sectors, 18 to 24 months to product-market fit is the norm, not the exception. Where technical complexity, customer validation, supply chain expertise and capital deployment patterns are fundamentally different from software.

Traditional VC due diligence wasn't built for these industries. Operators were.

Capital is moving, but allocators are still catching up

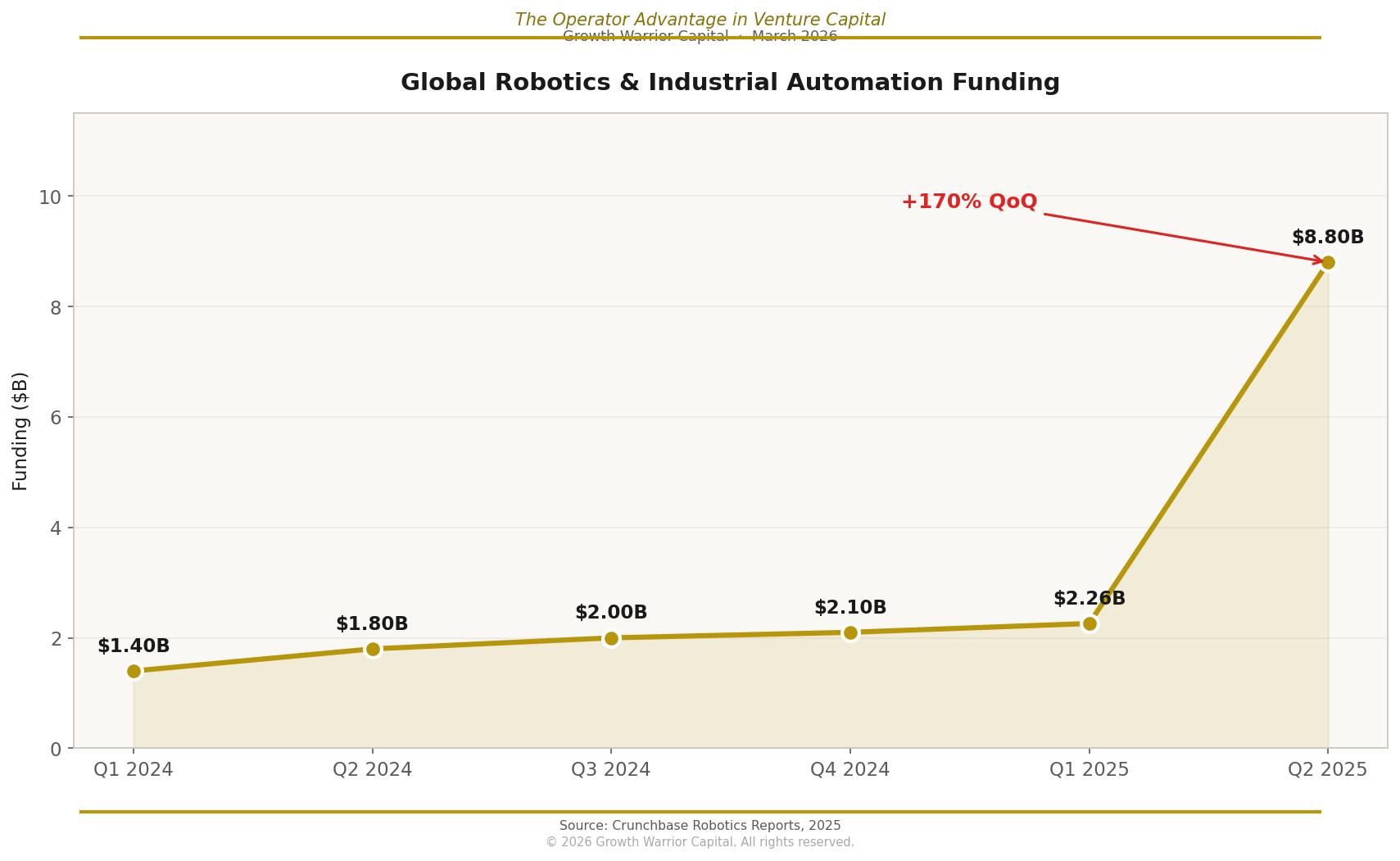

The robotics and industrial automation sector tells the story in capital flow terms.

Funding in this sector went from $1.4B in Q1 2024 to $8.8B in Q2 2025 — a 170% jump in a single quarter. The market is moving fast. Smart capital is already repositioning.

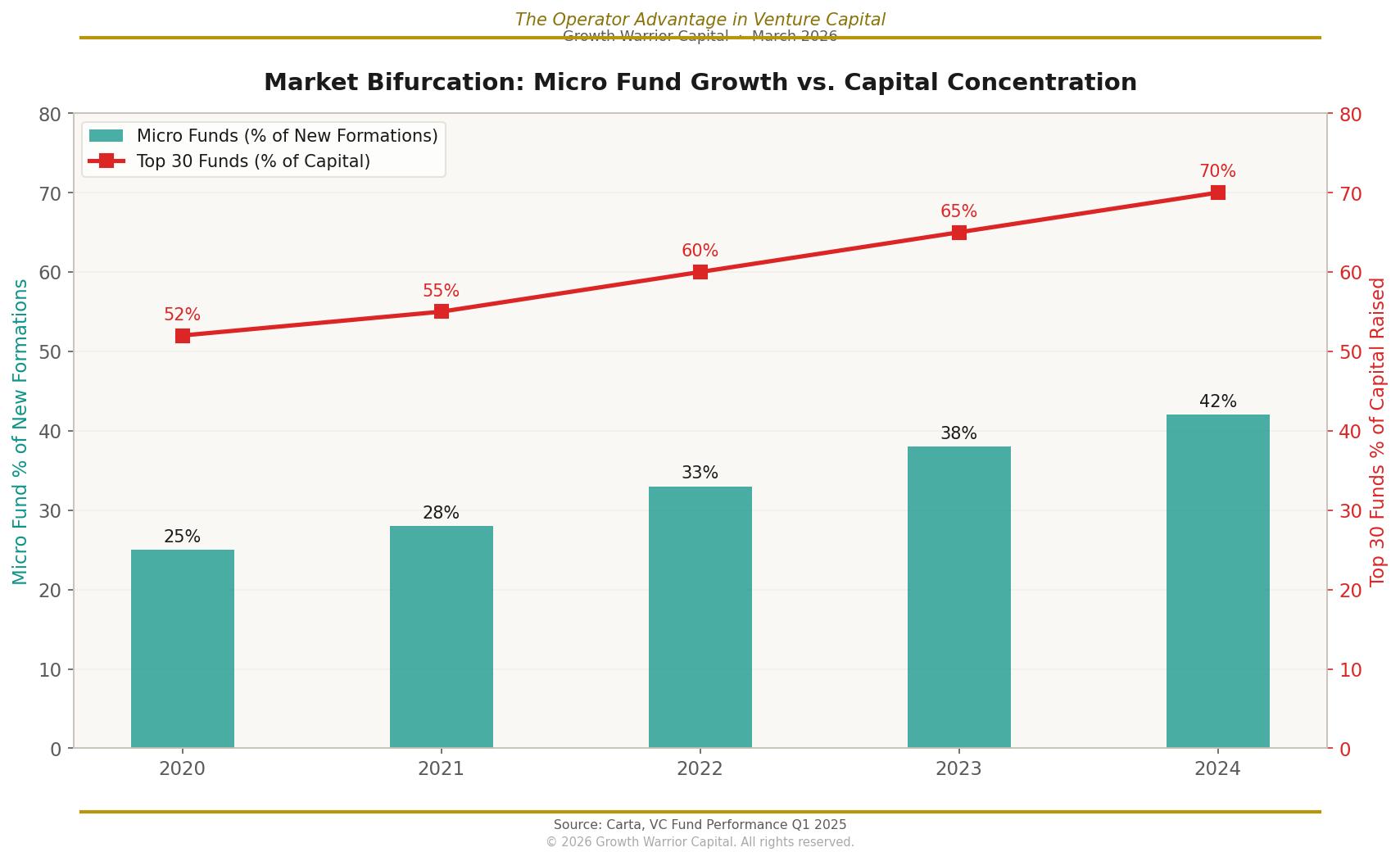

At the same time, the venture market itself is bifurcating in a way that creates a specific opening for emerging operator-led managers.

The top 30 funds now capture 70% of all venture capital — up from 52% in 2020. Micro fund formations have nearly doubled. The middle is hollowing out. For emerging managers with differentiated theses and operator credibility, this is exactly the environment where conviction-based investing wins.

The window for the Operator Advantage is still open

The data is clear. The structural advantage of operator-led investing is real, measurable and widening in the sectors where it matters most. Institutional allocators who recognize this early have an opportunity that won't exist at the same scale once the category is fully priced in.

Promise been building GWC around this thesis since 2021. Sheila's research is the most rigorous independent validation of it we've seen. We're sharing this data because the argument deserves to be made in full — with data, not just conviction.

Download the full whate paper at the end of this post.

----------

The views expressed in this post are those of Promise Phelon and Growth Warrior Capital as of March 2026. This content is for informational purposes only and does not constitute investment advice or a solicitation to invest in any fund. Please consult your professional advisors for investment decisions appropriate to your individual circumstances.

More From GWC

Back to All InsightsThe Operator Advantage in Venture Capital

Independent research from Scientifica.ai analyzed 87 operator-led funds and 124 traditional funds. The findings are unambiguous: Operator-led funds outperform traditional venture capital by 1.7x in early-stage returns. Here's what the data shows — and why the structural advantage is widest exactly where GWC operates.

.svg)